Today and tomorrow, we’re going to be taking a close look at how insurance companies have been doing since 1990 in appeals at the Supreme Court. Today, we’ll review the data about the types of cases the Court has heard, and insurers’ won-loss record year by year and overall, and tomorrow, we’ll be looking at the Justices’ individual voting records, and determining which Justices were more likely than the Court as a whole to vote in favor of insurer parties, and which Justices were less likely to.

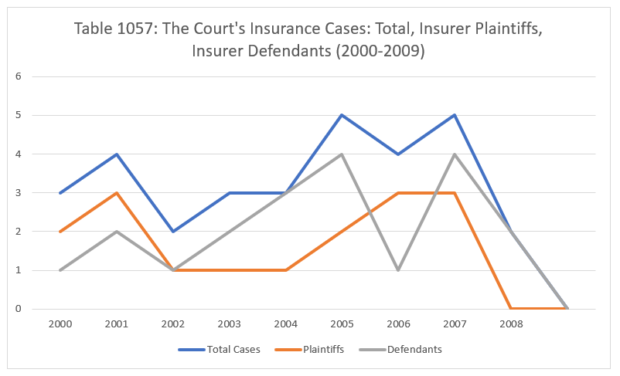

As a named party in litigation, insurers can be on either side of the “v.” – plaintiffs or defendants, depending on the issue involved. In Table 1056, we begin reviewing the data for (1) how many cases per year did the Court decided and (2) in how many was an insurer the plaintiff, and how many the defendant. Occasionally, the total of plaintiff plus defendant cases totals more than the “total cases” column – this represents cases in which an insurer was on both sides of the “v.”

During the nineties, the Court decided a total of forty-two cases primarily involving insurance law issues. That docket wasn’t a steady flow of cases from one year to the next; although the Court tended to decide three to four cases in most years, there were recurring spikes (total cases are tracked below in the blue line). The Court decided nine insurance cases in 1992 and seven in 1997. The Court decided only one insurance case in 1996. In most years, insurer defendants outnumbered insurer plaintiffs. For the nineties as a whole, 40.5% of insurer parties were plaintiffs to 59.5% defendants.

Between 2000 and 2009, the flow of insurance cases was a bit more predictable from year to year, albeit down a bit from the nineties. For the ten years, the Court decided thirty-three insurance cases in all. The spread between plaintiffs and defendants was closer too – 47.4% of the cases had insurer plaintiffs, 52.6% had insurer defendants (in this decade, there were several “insurer v. insurer” cases).

Since 2010, insurance law cases have continued to decline, as we see in Table 1058. Between 2010 and 2018, the Court has decided only thirteen insurance cases, including none in 2014, 2016 or 2017. For the first time, plaintiffs outnumbered defendants, with 69.23% of the cases involving an insurer plaintiff and only 30.77% an insurer defendant.

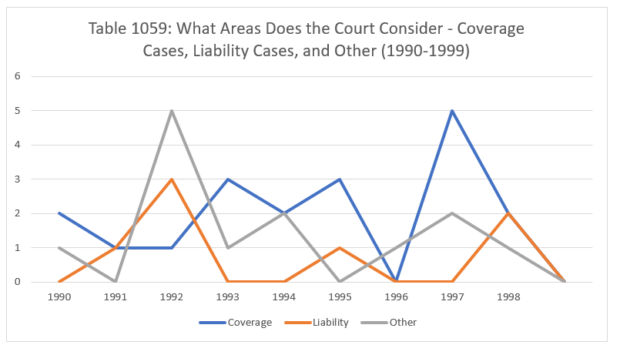

Next, let’s take a look at what these cases involved. Although our data on the areas of law involved in far more granular, broadly speaking, insurance cases can be divided into “coverage,” “liability” and “other.” In Table 1059, we follow the numbers for each group. Overall, between 1990 and 1999, the Court decided twenty-two coverage cases, only seven liability cases, and thirteen cases that were “other.”

Between 2000 and 2009, the Court decided twenty-seven cases dealing with coverage issues, five dealing with liability issues, and none in the “other” category.

The Court has decided almost no cases since 2010 involving anything other than coverage decisions. From 2010 to 2018, the Court has decided eleven coverage cases, one liability case, and no “other.”

Finally, we turn to the most fundamental statistic of all – the insurers’ win-loss record. Between 1990 and 1999, insurers have had a won-loss record at the Court of 25-17 – a winning percentage of 59.52%.

Between 2000 and 2009, things shifted a bit towards the insurers’ opponents. For the entire period, insurers had a won-loss record of 17-16. Between 1990 and 2009, insurers had a winning percentage at the Court of 56%.

Between 2010 and 2018, insurers’ winning percentage weakened at the Court. For those years, insurers were 5-8. For the entire period of 1990 to 2018, insurers were 47-41: a winning percentage of 53.41%.

Join us back here tomorrow as we turn our attention to the individual Justices’ voting records in insurance cases.

Image courtesy of Flickr by Tomosius (no changes).